Week of June 16

The World Turned Upside Down

The data last week was mostly benign, other than housing stars, which showed that residential construction continues to struggle in the face of high rates, a supply overhang in some areas, and concern over tariffs.

The U.S. strike on Iranian nuclear facilities, though, puts geopolitical risk at the top of concerns facing the U.S. economy. How this all shapes out in the coming days and weeks is unknown at this point, but it’s unlikely to be a one and done strike. Consumers and businesses were already nervous, and the threat of a wider conflict and potential run up in oil prices could easily push the economy over the edge and into a more pronounced slowdown – and yes, recession.

Important Data Points From The Past Week

U.S. Retail Sales

Total retail sales fell for the second consecutive month in May, falling 0.9% from April as consumers pared back their spending in the face of rising economic risk. Excluding autos, retail sales fell 0.3%.

On the downside, restaurant and food sales were down and building material sales posted a very large 2.7% drop from April. Nonstore (aka E-commerce) sales increased, as did sales at furniture, clothing, and sporting goods stores.

Consumers will likely continue to retrench as economic and geopolitical concerns impact confidence. This will push down overall economic growth over the coming two quarters.

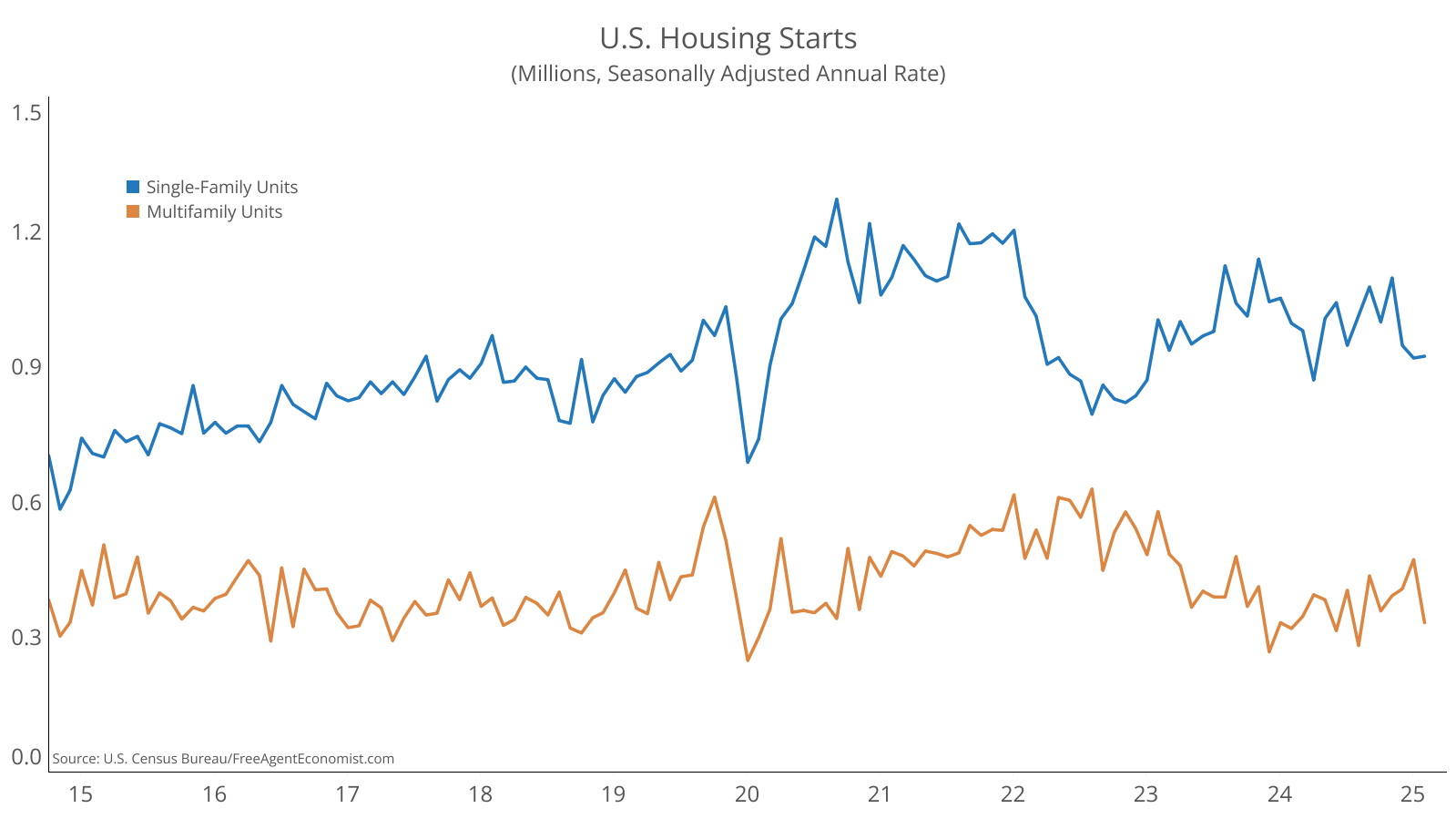

U.S. Housing Starts

Residential construction posted a significant drop in May, falling 9.8% over the month to a seasonally adjusted annual rate of 1.26 million units – the lowest level of activity since 2020. In May, multifamily construction fell nearly 30%, while single family starts were essentially flat.

Housing construction has been relatively healthy over the last year, despite high rates; however, the significant headwinds caused by tariff and broader macroeconomic and geopolitical concerns are proving to be too much to overcome.

Single family permits were down again in May and have dropped nearly 10% since February, suggesting that starts will be very weak over the coming months. This comes as unsold inventory has been ticking higher. Multifamily permits, though, have held up, suggesting better news for their future. Rising geopolitical tensions may thwart any significant rise, though. I’ve lowered my forecast for single family starts, but for now I continue to feel good about my multifamily outlook.

FOMC Meeting

The FOMC left interest rates unchanged at 4.25%-4.5% at their meeting last week. The press release noted, significantly, that “uncertainty about the economic outlook has diminished," but that it remains “elevated.”

Looking ahead, the FOMC is projecting two more rate cuts this year totaling 50 bps, although voting members appear to be split on two or three cuts. They are further suggesting that by the end of 2026 rates will be 100 bps lower than they currently are.

The split on two or three cuts this year feels right. There continues to be some uncertainty over how/when/if tariffs will impact broader inflation trends, and the labor market has bent but not broken. The current tension between Iran and Israel and the significant risk of increased U.S. involvement clouds this outlook. I think the Fed will act aggressively to cut rates should tariffs or external factors significantly weaken economic activity; and I think that leads to three cuts this year and not two.

Canadian Industrial Price Index

Canadian industrial prices fell in May, dropping 0.5% from April – the second consecutive monthly decline. Lumber prices slowed noticeably as demand has fallen in both the U.S. and Canadian housing markets. Energy prices were also lower, mostly due to lower prices for refined products like diesel fuel. On the flip side, non-ferrous metal prices were higher as gold prices moved higher due to its status as a safe haven in the current volatile economic landscape. Copper prices were also up as demand rose in the face of the U.S.-China trade cease fire.

Industrial prices should continue to cool as both the U.S. and Canadian economies slow. This will persist as long as trade tensions and global economic uncertainty persist.

Canadian Retail Sales

Canadian retail sales eked out an inflation-adjusted 0.5% increase in April over the previous month. Higher motor vehicle and gasoline sales were behind the increase, meaning that core retail sales were essentially flat. Food, building material, and clothing sales were all lower in the month, but were offset by gains in general merchandise, furniture and electronics, and sporting goods.

No news is good news in this data. Given the extreme pressure on the Canadian economy, a flat read on retail sales is good news. This April data, though, is somewhat ancient history and it’s likely that consumer spending slowed notably in May and through June.

What I’ll Be Watching This Week

Lots of interesting data coming down the road this week. In the U.S. we’ll see new home sales, two consumer confidence data points, durable goods, GDP and inflation data. In Canada, the main data point will be consumer inflation.

What I Listened To Last Week

I spent 16 hours in my car this week driving to Canada and back to take care of my parents and listened to this book. Hiaasen is always entertaining and this book at times was laugh out loud. The story follows his antihero Twilly Spree in his battle against corrupt Florida politicians.

How Can I Help?

I’m taking on a limited number of clients to help with bespoke analysis of the economy and construction and what it means for your company. I’m also available if you’re in need of a speaker at an event or someone to come talk to leadership groups on the state of the economy, demographics, real estate, and construction.

If you want to discuss either option, sign up for a spot on my calendar.

Do you know someone who would benefit from the information in this newsletter? Please share the sign up link with them.