Week of March 10

I don’t want to hear any more!

Is there any more?

Another week of intense news. The stock market was down, on again/off again tariffs, and now talk of recession! From my perspective, I think it’s way too early to make a recession call. The labor market is bending, but certainly not breaking. However, the uncertainty and confusion over the path of fiscal and trade policy has consumers and businesses very nervous and they will be pulling back their spending. As a result economic growth will slow to 1.4% this year from the 2.8% growth posted in 2024.

Facing this, there are two pieces of advice I would suggest you follow:

1. Turn off the news

2. Make sure you understand how leading indicators impact your business

Understanding this fundamental data will be your lifeboat during this storm and if done right will give you good lead time to upcoming periods of growth and contraction. This should be an important element of your business strategy.

If you need help in building this out, please set up a time to chat!

Important Data Points From The Past Week

U.S. Consumer Price Index

Inflation cooled in February; good news after the hotter-than-expected read in January. On a year-over-year basis, headline consumer inflation slowed from 3.0% to 2.8%, core inflation (less food and energy) eased from 3.3% to 3.1% and supercore (less food, energy, and shelter) slowed from 2.2% to 2.1%.

There were mixed results on the building product side. There was further erosion in prices for floor and window coverings, but the other categories saw price acceleration. Given that these are consumer-facing prices it’s hard to suss out exactly what’s happening here. Are tariffs impacting consumer prices? Price discounting? Or is it demand related? I think it’s unlikely that tariffs are at play here. This is data from February and that would be too early. I think the other factors are at play here, and with consumer spending slated to ease along with home improvement activities, I think we’ll see more discounts and lower prices throughout the year.

From the Fed’s perspective, while this isn’t their preferred measure of inflation it probably allows them to breathe a little easier and allow rates to stay where they are until they get a better read on tariffs and the slowing economy.

Canadian Monetary Policy

The Bank of Canada cut its benchmark rate by 25 basis points on Tuesday, mostly likely a prophylactic move to stave off the negative implications of US tariffs. The Canadian economy ended last year on a pretty solid note and Q1 will likely see another solid read due to increased exports to the U.S. from stockpiling.

The way I read this is that the Bank clearly views the potential for a slowing economy more risky than inflation. Following that logic you should expect another cut or two before summer is over.

U.S. Producer Price Index

Much like the consumer inflation read, wholesale price inflation also eased in February with the final demand measure slowing from 3.7% year-over-year to 3.2% and the core measure slipping from 2.3% to 1.7%. Eggs were one of the largest price increases in the data (they jumped 54%). On the other hand, gas prices fell 4.7%.

On the construction front, inputs to new construction remained pretty steady from January to February, with the only exceptions being new healthcare and industrial structures. So far my forecasts (click here for the table) for 2025 are on track, showing accelerations in construction materials and new residential construction. Prices for new nonresidential are expected to be flat-ish this year, but with all of these prices tariffs could have a profound impact. The question would be: will quickening inflation from tariffs be offset by the reduced demand that tariffs will cause? For now, I’m leaning towards no. Even if tariffs stick we should still see strong demand for data centers and infrastructure, which will keep demand for materials strong.

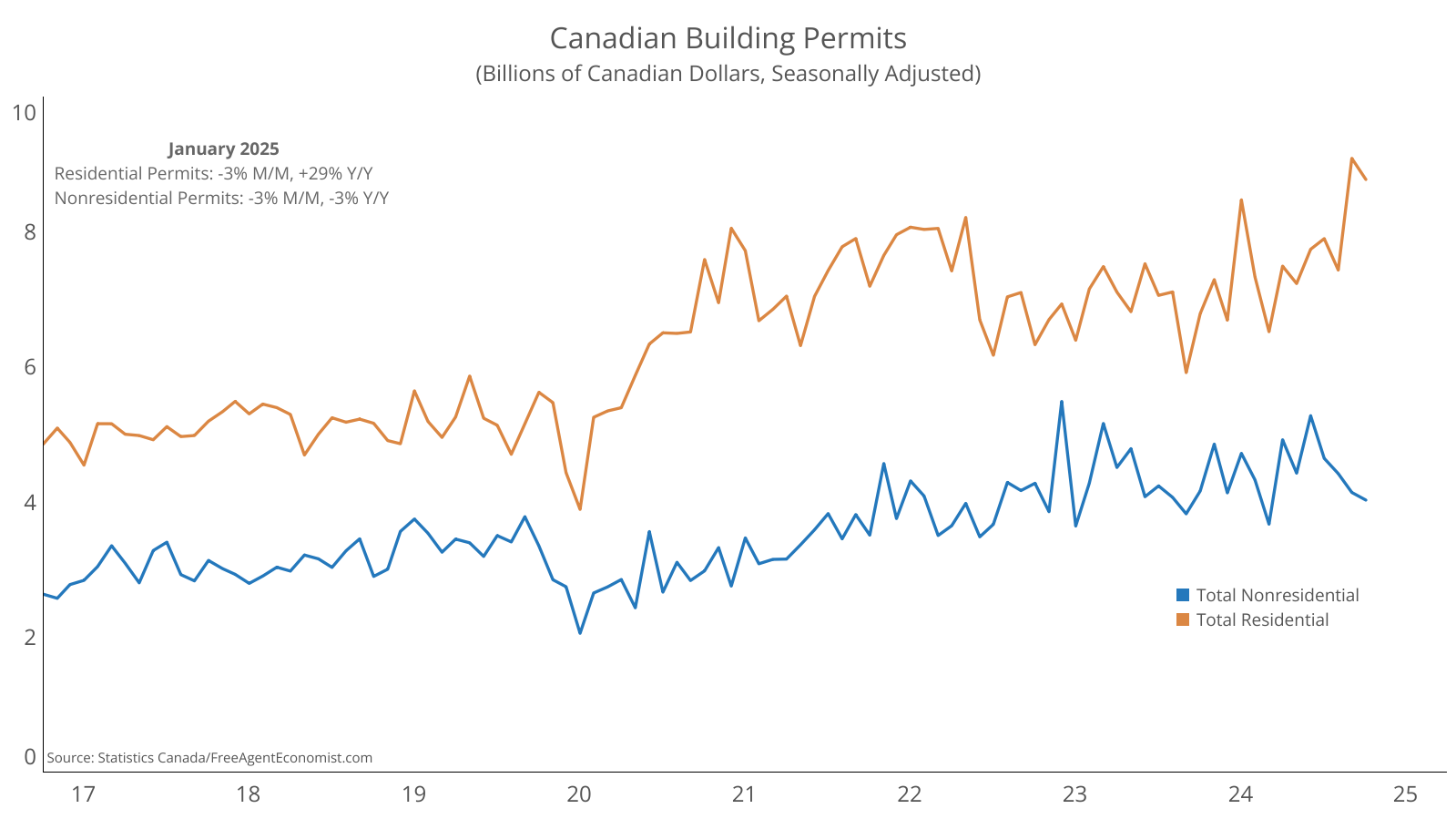

Canadian Building Permits

Canadian building permits fell in January, slipping 3.2% to $12.8 billion CDN. Residential permits were down 3% due to multifamily; nonresidential permits also lost 3% due to declines in industrial and institutional.

The Canadian permit data can be pretty volatile when you look at it monthly, but if you look at rolling 12 months there is a definite acceleration happening led mostly by residential and commercial. Will that last? I’m forecasting total permits to be up 3% for 2025 (click here for the forecast table). Expect that slowdown to hit by summer.

What I’ll Be Watching This Week

What won’t I be watching?! It’s a busy data week – in the U.S. there are retail sales, housing data, industrial production, and a Fed meeting. Housing data in Canada as well, plus two important inflation reads.

What I Watched Last Week

This WWII epic tells the story of Operation Market Garden – a failed allied plan in the Netherlands in 1944. There are a lot of big name actors in it, but at its essence it highlights individual bravery combined with leadership that refused to see from the underlying data that the mission was set to fail before it even started. Can you see the theme this week?

By the way, the title of the newsletter is from a conversation in the movie as the bad news mounts.

How Can I Help?

I’m taking on a limited number of clients to help with bespoke analysis of the economy and construction and what it means for your company. I’m also available if you’re in need of a speaker at an event or someone to come talk to leadership groups on the state of the economy, demographics, real estate, and construction.

If you want to discuss either option, sign up for a spot on my calendar.

Do you know someone who would benefit from the information in this newsletter? Please share the sign up link with them.